import warnings

warnings.filterwarnings('ignore')

import numpy as np

import pandas as pd

np.random.seed(12345)

import matplotlib.pyplot as plt

plt.rc("figure", figsize=(10, 6))

PREVIOUS_MAX_ROWS = pd.options.display.max_rows

pd.options.display.max_columns = 20

pd.options.display.max_rows = 20

pd.options.display.max_colwidth = 80

np.set_printoptions(precision=4, suppress=True)

import matplotlib.pyplot as plt

# Matplotlib 한글 폰트 설정 (macOS용)

plt.rc('font', family='AppleGothic')

plt.rc('axes', unicode_minus=False)10 11장: 시계열

시간의 흐름에 따른 데이터를 분석하기 위한 시계열 특화 기능을 학습합니다.

import numpy as np

import pandas as pd10.1 날짜, 시간 자료형, 도구

파이썬 내장 datetime 라이브러리와 pandas의 시간 도구들을 비교합니다.

10.2 날짜와 시간 시스템

파이썬의 표준 시간 도구와 pandas의 차이점을 인지합니다.

from datetime import datetime

now = datetime.now()

now

now.year, now.month, now.day(2026, 2, 26)delta = datetime(2011, 1, 7) - datetime(2008, 6, 24, 8, 15)

delta

delta.days

delta.seconds56700from datetime import timedelta

start = datetime(2011, 1, 7)

start + timedelta(12)

start - 2 * timedelta(12)datetime.datetime(2010, 12, 14, 0, 0)stamp = datetime(2011, 1, 3)

str(stamp)

stamp.strftime("%Y-%m-%d")'2011-01-03'value = "2011-01-03"

datetime.strptime(value, "%Y-%m-%d")

datestrs = ["7/6/2011", "8/6/2011"]

[datetime.strptime(x, "%m/%d/%Y") for x in datestrs][datetime.datetime(2011, 7, 6, 0, 0), datetime.datetime(2011, 8, 6, 0, 0)]datestrs = ["2011-07-06 12:00:00", "2011-08-06 00:00:00"]

pd.to_datetime(datestrs)DatetimeIndex(['2011-07-06 12:00:00', '2011-08-06 00:00:00'], dtype='datetime64[ns]', freq=None)idx = pd.to_datetime(datestrs + [None])

idx

idx[2]

pd.isna(idx)array([False, False, True])10.3 시계열 기초

날짜를 색인으로 사용하는 시계열 객체의 생성과 활용을 배웁니다.

dates = [datetime(2011, 1, 2), datetime(2011, 1, 5),

datetime(2011, 1, 7), datetime(2011, 1, 8),

datetime(2011, 1, 10), datetime(2011, 1, 12)]

ts = pd.Series(np.random.standard_normal(6), index=dates)

ts2011-01-02 -0.204708

2011-01-05 0.478943

2011-01-07 -0.519439

2011-01-08 -0.555730

2011-01-10 1.965781

2011-01-12 1.393406

dtype: float6410.4 시계열 기초

시간을 색인으로 사용하는 Series와 DataFrame을 다루는 방법을 알아봅니다.

ts.indexDatetimeIndex(['2011-01-02', '2011-01-05', '2011-01-07', '2011-01-08',

'2011-01-10', '2011-01-12'],

dtype='datetime64[ns]', freq=None)ts + ts[::2]2011-01-02 -0.409415

2011-01-05 NaN

2011-01-07 -1.038877

2011-01-08 NaN

2011-01-10 3.931561

2011-01-12 NaN

dtype: float64ts.index.dtypedtype('<M8[ns]')stamp = ts.index[0]

stampTimestamp('2011-01-02 00:00:00')stamp = ts.index[2]

ts[stamp]-0.5194387150567381ts["2011-01-10"]1.9657805725027142longer_ts = pd.Series(np.random.standard_normal(1000),

index=pd.date_range("2000-01-01", periods=1000))

longer_ts

longer_ts["2001"]2001-01-01 1.599534

2001-01-02 0.474071

2001-01-03 0.151326

2001-01-04 -0.542173

2001-01-05 -0.475496

...

2001-12-27 0.057874

2001-12-28 -0.433739

2001-12-29 0.092698

2001-12-30 -1.397820

2001-12-31 1.457823

Freq: D, Length: 365, dtype: float64longer_ts["2001-05"]2001-05-01 -0.622547

2001-05-02 0.936289

2001-05-03 0.750018

2001-05-04 -0.056715

2001-05-05 2.300675

...

2001-05-27 0.235477

2001-05-28 0.111835

2001-05-29 -1.251504

2001-05-30 -2.949343

2001-05-31 0.634634

Freq: D, Length: 31, dtype: float64ts[datetime(2011, 1, 7):]

ts[datetime(2011, 1, 7):datetime(2011, 1, 10)]2011-01-07 -0.519439

2011-01-08 -0.555730

2011-01-10 1.965781

dtype: float64ts

ts["2011-01-06":"2011-01-11"]2011-01-07 -0.519439

2011-01-08 -0.555730

2011-01-10 1.965781

dtype: float64ts.truncate(after="2011-01-09")2011-01-02 -0.204708

2011-01-05 0.478943

2011-01-07 -0.519439

2011-01-08 -0.555730

dtype: float64dates = pd.date_range("2000-01-01", periods=100, freq="W-WED")

long_df = pd.DataFrame(np.random.standard_normal((100, 4)),

index=dates,

columns=["Colorado", "Texas",

"New York", "Ohio"])

long_df.loc["2001-05"]| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2001-05-02 | -0.006045 | 0.490094 | -0.277186 | -0.707213 |

| 2001-05-09 | -0.560107 | 2.735527 | 0.927335 | 1.513906 |

| 2001-05-16 | 0.538600 | 1.273768 | 0.667876 | -0.969206 |

| 2001-05-23 | 1.676091 | -0.817649 | 0.050188 | 1.951312 |

| 2001-05-30 | 3.260383 | 0.963301 | 1.201206 | -1.852001 |

dates = pd.DatetimeIndex(["2000-01-01", "2000-01-02", "2000-01-02",

"2000-01-02", "2000-01-03"])

dup_ts = pd.Series(np.arange(5), index=dates)

dup_ts2000-01-01 0

2000-01-02 1

2000-01-02 2

2000-01-02 3

2000-01-03 4

dtype: int64dup_ts.index.is_uniqueFalsedup_ts["2000-01-03"] # not duplicated

dup_ts["2000-01-02"] # duplicated2000-01-02 1

2000-01-02 2

2000-01-02 3

dtype: int64grouped = dup_ts.groupby(level=0)

grouped.mean()

grouped.count()2000-01-01 1

2000-01-02 3

2000-01-03 1

dtype: int64ts

resampler = ts.resample("D")

resampler<pandas.core.resample.DatetimeIndexResampler object at 0x15506a910>index = pd.date_range("2012-04-01", "2012-06-01")

indexDatetimeIndex(['2012-04-01', '2012-04-02', '2012-04-03', '2012-04-04',

'2012-04-05', '2012-04-06', '2012-04-07', '2012-04-08',

'2012-04-09', '2012-04-10', '2012-04-11', '2012-04-12',

'2012-04-13', '2012-04-14', '2012-04-15', '2012-04-16',

'2012-04-17', '2012-04-18', '2012-04-19', '2012-04-20',

'2012-04-21', '2012-04-22', '2012-04-23', '2012-04-24',

'2012-04-25', '2012-04-26', '2012-04-27', '2012-04-28',

'2012-04-29', '2012-04-30', '2012-05-01', '2012-05-02',

'2012-05-03', '2012-05-04', '2012-05-05', '2012-05-06',

'2012-05-07', '2012-05-08', '2012-05-09', '2012-05-10',

'2012-05-11', '2012-05-12', '2012-05-13', '2012-05-14',

'2012-05-15', '2012-05-16', '2012-05-17', '2012-05-18',

'2012-05-19', '2012-05-20', '2012-05-21', '2012-05-22',

'2012-05-23', '2012-05-24', '2012-05-25', '2012-05-26',

'2012-05-27', '2012-05-28', '2012-05-29', '2012-05-30',

'2012-05-31', '2012-06-01'],

dtype='datetime64[ns]', freq='D')10.5 날짜 범위, 빈도, 이동

빈도를 지정하여 날짜 범위를 생성하거나 데이터를 앞뒤로 밀어내는 방법(shift)을 배웁니다.

pd.date_range(start="2012-04-01", periods=20)

pd.date_range(end="2012-06-01", periods=20)DatetimeIndex(['2012-05-13', '2012-05-14', '2012-05-15', '2012-05-16',

'2012-05-17', '2012-05-18', '2012-05-19', '2012-05-20',

'2012-05-21', '2012-05-22', '2012-05-23', '2012-05-24',

'2012-05-25', '2012-05-26', '2012-05-27', '2012-05-28',

'2012-05-29', '2012-05-30', '2012-05-31', '2012-06-01'],

dtype='datetime64[ns]', freq='D')pd.date_range("2000-01-01", "2000-12-01", freq="BM")DatetimeIndex(['2000-01-31', '2000-02-29', '2000-03-31', '2000-04-28',

'2000-05-31', '2000-06-30', '2000-07-31', '2000-08-31',

'2000-09-29', '2000-10-31', '2000-11-30'],

dtype='datetime64[ns]', freq='BM')pd.date_range("2012-05-02 12:56:31", periods=5)DatetimeIndex(['2012-05-02 12:56:31', '2012-05-03 12:56:31',

'2012-05-04 12:56:31', '2012-05-05 12:56:31',

'2012-05-06 12:56:31'],

dtype='datetime64[ns]', freq='D')pd.date_range("2012-05-02 12:56:31", periods=5, normalize=True)DatetimeIndex(['2012-05-02', '2012-05-03', '2012-05-04', '2012-05-05',

'2012-05-06'],

dtype='datetime64[ns]', freq='D')from pandas.tseries.offsets import Hour, Minute

hour = Hour()

hour<Hour>four_hours = Hour(4)

four_hours<4 * Hours>pd.date_range("2000-01-01", "2000-01-03 23:59", freq="4H")DatetimeIndex(['2000-01-01 00:00:00', '2000-01-01 04:00:00',

'2000-01-01 08:00:00', '2000-01-01 12:00:00',

'2000-01-01 16:00:00', '2000-01-01 20:00:00',

'2000-01-02 00:00:00', '2000-01-02 04:00:00',

'2000-01-02 08:00:00', '2000-01-02 12:00:00',

'2000-01-02 16:00:00', '2000-01-02 20:00:00',

'2000-01-03 00:00:00', '2000-01-03 04:00:00',

'2000-01-03 08:00:00', '2000-01-03 12:00:00',

'2000-01-03 16:00:00', '2000-01-03 20:00:00'],

dtype='datetime64[ns]', freq='4H')Hour(2) + Minute(30)<150 * Minutes>pd.date_range("2000-01-01", periods=10, freq="1h30min")DatetimeIndex(['2000-01-01 00:00:00', '2000-01-01 01:30:00',

'2000-01-01 03:00:00', '2000-01-01 04:30:00',

'2000-01-01 06:00:00', '2000-01-01 07:30:00',

'2000-01-01 09:00:00', '2000-01-01 10:30:00',

'2000-01-01 12:00:00', '2000-01-01 13:30:00'],

dtype='datetime64[ns]', freq='90T')monthly_dates = pd.date_range("2012-01-01", "2012-09-01", freq="WOM-3FRI")

list(monthly_dates)[Timestamp('2012-01-20 00:00:00'),

Timestamp('2012-02-17 00:00:00'),

Timestamp('2012-03-16 00:00:00'),

Timestamp('2012-04-20 00:00:00'),

Timestamp('2012-05-18 00:00:00'),

Timestamp('2012-06-15 00:00:00'),

Timestamp('2012-07-20 00:00:00'),

Timestamp('2012-08-17 00:00:00')]10.6 데이터 이동과 빈도

시간축을 따라 데이터를 앞뒤로 이동시키는 연산을 수행합니다.

ts = pd.Series(np.random.standard_normal(4),

index=pd.date_range("2000-01-01", periods=4, freq="M"))

ts

ts.shift(2)

ts.shift(-2)2000-01-31 -0.117388

2000-02-29 -0.517795

2000-03-31 NaN

2000-04-30 NaN

Freq: M, dtype: float64ts.shift(2, freq="M")2000-03-31 -0.066748

2000-04-30 0.838639

2000-05-31 -0.117388

2000-06-30 -0.517795

Freq: M, dtype: float64ts.shift(3, freq="D")

ts.shift(1, freq="90T")2000-01-31 01:30:00 -0.066748

2000-02-29 01:30:00 0.838639

2000-03-31 01:30:00 -0.117388

2000-04-30 01:30:00 -0.517795

dtype: float64from pandas.tseries.offsets import Day, MonthEnd

now = datetime(2011, 11, 17)

now + 3 * Day()Timestamp('2011-11-20 00:00:00')now + MonthEnd()

now + MonthEnd(2)Timestamp('2011-12-31 00:00:00')offset = MonthEnd()

offset.rollforward(now)

offset.rollback(now)Timestamp('2011-10-31 00:00:00')ts = pd.Series(np.random.standard_normal(20),

index=pd.date_range("2000-01-15", periods=20, freq="4D"))

ts

ts.groupby(MonthEnd().rollforward).mean()2000-01-31 -0.005833

2000-02-29 0.015894

2000-03-31 0.150209

dtype: float64ts.resample("M").mean()2000-01-31 -0.005833

2000-02-29 0.015894

2000-03-31 0.150209

Freq: M, dtype: float64import pytz

pytz.common_timezones[-5:]['US/Eastern', 'US/Hawaii', 'US/Mountain', 'US/Pacific', 'UTC']10.7 시간대 처리

국제화된 데이터를 다루기 위한 시간대(time zone) 변환 작업을 수행합니다.

tz = pytz.timezone("America/New_York")

tz<DstTzInfo 'America/New_York' LMT-1 day, 19:04:00 STD>dates = pd.date_range("2012-03-09 09:30", periods=6)

ts = pd.Series(np.random.standard_normal(len(dates)), index=dates)

ts2012-03-09 09:30:00 -0.202469

2012-03-10 09:30:00 0.050718

2012-03-11 09:30:00 0.639869

2012-03-12 09:30:00 0.597594

2012-03-13 09:30:00 -0.797246

2012-03-14 09:30:00 0.472879

Freq: D, dtype: float64print(ts.index.tz)Nonepd.date_range("2012-03-09 09:30", periods=10, tz="UTC")DatetimeIndex(['2012-03-09 09:30:00+00:00', '2012-03-10 09:30:00+00:00',

'2012-03-11 09:30:00+00:00', '2012-03-12 09:30:00+00:00',

'2012-03-13 09:30:00+00:00', '2012-03-14 09:30:00+00:00',

'2012-03-15 09:30:00+00:00', '2012-03-16 09:30:00+00:00',

'2012-03-17 09:30:00+00:00', '2012-03-18 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq='D')10.8 시간대 처리

글로벌 데이터를 분석할 때 필수적인 시간대 변환 기법을 알아봅니다.

ts

ts_utc = ts.tz_localize("UTC")

ts_utc

ts_utc.indexDatetimeIndex(['2012-03-09 09:30:00+00:00', '2012-03-10 09:30:00+00:00',

'2012-03-11 09:30:00+00:00', '2012-03-12 09:30:00+00:00',

'2012-03-13 09:30:00+00:00', '2012-03-14 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq='D')ts_utc.tz_convert("America/New_York")2012-03-09 04:30:00-05:00 -0.202469

2012-03-10 04:30:00-05:00 0.050718

2012-03-11 05:30:00-04:00 0.639869

2012-03-12 05:30:00-04:00 0.597594

2012-03-13 05:30:00-04:00 -0.797246

2012-03-14 05:30:00-04:00 0.472879

Freq: D, dtype: float64ts_eastern = ts.tz_localize("America/New_York")

ts_eastern.tz_convert("UTC")

ts_eastern.tz_convert("Europe/Berlin")2012-03-09 15:30:00+01:00 -0.202469

2012-03-10 15:30:00+01:00 0.050718

2012-03-11 14:30:00+01:00 0.639869

2012-03-12 14:30:00+01:00 0.597594

2012-03-13 14:30:00+01:00 -0.797246

2012-03-14 14:30:00+01:00 0.472879

dtype: float64ts.index.tz_localize("Asia/Shanghai")DatetimeIndex(['2012-03-09 09:30:00+08:00', '2012-03-10 09:30:00+08:00',

'2012-03-11 09:30:00+08:00', '2012-03-12 09:30:00+08:00',

'2012-03-13 09:30:00+08:00', '2012-03-14 09:30:00+08:00'],

dtype='datetime64[ns, Asia/Shanghai]', freq=None)stamp = pd.Timestamp("2011-03-12 04:00")

stamp_utc = stamp.tz_localize("utc")

stamp_utc.tz_convert("America/New_York")Timestamp('2011-03-11 23:00:00-0500', tz='America/New_York')stamp_moscow = pd.Timestamp("2011-03-12 04:00", tz="Europe/Moscow")

stamp_moscowTimestamp('2011-03-12 04:00:00+0300', tz='Europe/Moscow')stamp_utc.value

stamp_utc.tz_convert("America/New_York").value1299902400000000000stamp = pd.Timestamp("2012-03-11 01:30", tz="US/Eastern")

stamp

stamp + Hour()Timestamp('2012-03-11 03:30:00-0400', tz='US/Eastern')stamp = pd.Timestamp("2012-11-04 00:30", tz="US/Eastern")

stamp

stamp + 2 * Hour()Timestamp('2012-11-04 01:30:00-0500', tz='US/Eastern')dates = pd.date_range("2012-03-07 09:30", periods=10, freq="B")

ts = pd.Series(np.random.standard_normal(len(dates)), index=dates)

ts

ts1 = ts[:7].tz_localize("Europe/London")

ts2 = ts1[2:].tz_convert("Europe/Moscow")

result = ts1 + ts2

result.indexDatetimeIndex(['2012-03-07 09:30:00+00:00', '2012-03-08 09:30:00+00:00',

'2012-03-09 09:30:00+00:00', '2012-03-12 09:30:00+00:00',

'2012-03-13 09:30:00+00:00', '2012-03-14 09:30:00+00:00',

'2012-03-15 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq=None)p = pd.Period("2011", freq="A-DEC")

pPeriod('2011', 'A-DEC')p + 5

p - 2Period('2009', 'A-DEC')pd.Period("2014", freq="A-DEC") - p<3 * YearEnds: month=12>periods = pd.period_range("2000-01-01", "2000-06-30", freq="M")

periodsPeriodIndex(['2000-01', '2000-02', '2000-03', '2000-04', '2000-05', '2000-06'], dtype='period[M]')pd.Series(np.random.standard_normal(6), index=periods)2000-01 -0.514551

2000-02 -0.559782

2000-03 -0.783408

2000-04 -1.797685

2000-05 -0.172670

2000-06 0.680215

Freq: M, dtype: float64values = ["2001Q3", "2002Q2", "2003Q1"]

index = pd.PeriodIndex(values, freq="Q-DEC")

indexPeriodIndex(['2001Q3', '2002Q2', '2003Q1'], dtype='period[Q-DEC]')p = pd.Period("2011", freq="A-DEC")

p

p.asfreq("M", how="start")

p.asfreq("M", how="end")

p.asfreq("M")Period('2011-12', 'M')p = pd.Period("2011", freq="A-JUN")

p

p.asfreq("M", how="start")

p.asfreq("M", how="end")Period('2011-06', 'M')p = pd.Period("Aug-2011", "M")

p.asfreq("A-JUN")Period('2012', 'A-JUN')periods = pd.period_range("2006", "2009", freq="A-DEC")

ts = pd.Series(np.random.standard_normal(len(periods)), index=periods)

ts

ts.asfreq("M", how="start")2006-01 1.607578

2007-01 0.200381

2008-01 -0.834068

2009-01 -0.302988

Freq: M, dtype: float64ts.asfreq("B", how="end")2006-12-29 1.607578

2007-12-31 0.200381

2008-12-31 -0.834068

2009-12-31 -0.302988

Freq: B, dtype: float64p = pd.Period("2012Q4", freq="Q-JAN")

pPeriod('2012Q4', 'Q-JAN')p.asfreq("D", how="start")

p.asfreq("D", how="end")Period('2012-01-31', 'D')p4pm = (p.asfreq("B", how="end") - 1).asfreq("T", how="start") + 16 * 60

p4pm

p4pm.to_timestamp()Timestamp('2012-01-30 16:00:00')periods = pd.period_range("2011Q3", "2012Q4", freq="Q-JAN")

ts = pd.Series(np.arange(len(periods)), index=periods)

ts

new_periods = (periods.asfreq("B", "end") - 1).asfreq("H", "start") + 16

ts.index = new_periods.to_timestamp()

ts2010-10-28 16:00:00 0

2011-01-28 16:00:00 1

2011-04-28 16:00:00 2

2011-07-28 16:00:00 3

2011-10-28 16:00:00 4

2012-01-30 16:00:00 5

dtype: int64dates = pd.date_range("2000-01-01", periods=3, freq="M")

ts = pd.Series(np.random.standard_normal(3), index=dates)

ts

pts = ts.to_period()

pts2000-01 1.663261

2000-02 -0.996206

2000-03 1.521760

Freq: M, dtype: float64dates = pd.date_range("2000-01-29", periods=6)

ts2 = pd.Series(np.random.standard_normal(6), index=dates)

ts2

ts2.to_period("M")2000-01 0.244175

2000-01 0.423331

2000-01 -0.654040

2000-02 2.089154

2000-02 -0.060220

2000-02 -0.167933

Freq: M, dtype: float64pts = ts2.to_period()

pts

pts.to_timestamp(how="end")2000-01-29 23:59:59.999999999 0.244175

2000-01-30 23:59:59.999999999 0.423331

2000-01-31 23:59:59.999999999 -0.654040

2000-02-01 23:59:59.999999999 2.089154

2000-02-02 23:59:59.999999999 -0.060220

2000-02-03 23:59:59.999999999 -0.167933

Freq: D, dtype: float64data = pd.read_csv("examples/macrodata.csv")

data.head(5)

data["year"]

data["quarter"]0 1

1 2

2 3

3 4

4 1

..

198 3

199 4

200 1

201 2

202 3

Name: quarter, Length: 203, dtype: int64index = pd.PeriodIndex(year=data["year"], quarter=data["quarter"],

freq="Q-DEC")

index

data.index = index

data["infl"]1959Q1 0.00

1959Q2 2.34

1959Q3 2.74

1959Q4 0.27

1960Q1 2.31

...

2008Q3 -3.16

2008Q4 -8.79

2009Q1 0.94

2009Q2 3.37

2009Q3 3.56

Freq: Q-DEC, Name: infl, Length: 203, dtype: float64dates = pd.date_range("2000-01-01", periods=100)

ts = pd.Series(np.random.standard_normal(len(dates)), index=dates)

ts

ts.resample("M").mean()

ts.resample("M", kind="period").mean()2000-01 -0.165893

2000-02 0.078606

2000-03 0.223811

2000-04 -0.063643

Freq: M, dtype: float64dates = pd.date_range("2000-01-01", periods=12, freq="T")

ts = pd.Series(np.arange(len(dates)), index=dates)

ts2000-01-01 00:00:00 0

2000-01-01 00:01:00 1

2000-01-01 00:02:00 2

2000-01-01 00:03:00 3

2000-01-01 00:04:00 4

2000-01-01 00:05:00 5

2000-01-01 00:06:00 6

2000-01-01 00:07:00 7

2000-01-01 00:08:00 8

2000-01-01 00:09:00 9

2000-01-01 00:10:00 10

2000-01-01 00:11:00 11

Freq: T, dtype: int64ts.resample("5min").sum()2000-01-01 00:00:00 10

2000-01-01 00:05:00 35

2000-01-01 00:10:00 21

Freq: 5T, dtype: int64ts.resample("5min", closed="right").sum()1999-12-31 23:55:00 0

2000-01-01 00:00:00 15

2000-01-01 00:05:00 40

2000-01-01 00:10:00 11

Freq: 5T, dtype: int64ts.resample("5min", closed="right", label="right").sum()2000-01-01 00:00:00 0

2000-01-01 00:05:00 15

2000-01-01 00:10:00 40

2000-01-01 00:15:00 11

Freq: 5T, dtype: int64from pandas.tseries.frequencies import to_offset

result = ts.resample("5min", closed="right", label="right").sum()

result.index = result.index + to_offset("-1s")

result1999-12-31 23:59:59 0

2000-01-01 00:04:59 15

2000-01-01 00:09:59 40

2000-01-01 00:14:59 11

Freq: 5T, dtype: int64ts = pd.Series(np.random.permutation(np.arange(len(dates))), index=dates)

ts.resample("5min").ohlc()| open | high | low | close | |

|---|---|---|---|---|

| 2000-01-01 00:00:00 | 8 | 8 | 1 | 5 |

| 2000-01-01 00:05:00 | 6 | 11 | 2 | 2 |

| 2000-01-01 00:10:00 | 0 | 7 | 0 | 7 |

frame = pd.DataFrame(np.random.standard_normal((2, 4)),

index=pd.date_range("2000-01-01", periods=2,

freq="W-WED"),

columns=["Colorado", "Texas", "New York", "Ohio"])

frame| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-05 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-12 | 0.493841 | -0.155434 | 1.397286 | 1.507055 |

df_daily = frame.resample("D").asfreq()

df_daily| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-05 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-06 | NaN | NaN | NaN | NaN |

| 2000-01-07 | NaN | NaN | NaN | NaN |

| 2000-01-08 | NaN | NaN | NaN | NaN |

| 2000-01-09 | NaN | NaN | NaN | NaN |

| 2000-01-10 | NaN | NaN | NaN | NaN |

| 2000-01-11 | NaN | NaN | NaN | NaN |

| 2000-01-12 | 0.493841 | -0.155434 | 1.397286 | 1.507055 |

frame.resample("D").ffill()| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-05 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-06 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-07 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-08 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-09 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-10 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-11 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-12 | 0.493841 | -0.155434 | 1.397286 | 1.507055 |

frame.resample("D").ffill(limit=2)| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-05 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-06 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-07 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-08 | NaN | NaN | NaN | NaN |

| 2000-01-09 | NaN | NaN | NaN | NaN |

| 2000-01-10 | NaN | NaN | NaN | NaN |

| 2000-01-11 | NaN | NaN | NaN | NaN |

| 2000-01-12 | 0.493841 | -0.155434 | 1.397286 | 1.507055 |

frame.resample("W-THU").ffill()| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-06 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-13 | 0.493841 | -0.155434 | 1.397286 | 1.507055 |

frame = pd.DataFrame(np.random.standard_normal((24, 4)),

index=pd.period_range("1-2000", "12-2001",

freq="M"),

columns=["Colorado", "Texas", "New York", "Ohio"])

frame.head()

annual_frame = frame.resample("A-DEC").mean()

annual_frame| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

# Q-DEC: Quarterly, year ending in December

annual_frame.resample("Q-DEC").ffill()

annual_frame.resample("Q-DEC", convention="end").asfreq()| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000Q4 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q1 | NaN | NaN | NaN | NaN |

| 2001Q2 | NaN | NaN | NaN | NaN |

| 2001Q3 | NaN | NaN | NaN | NaN |

| 2001Q4 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

annual_frame.resample("Q-MAR").ffill()| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000Q4 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q1 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q2 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q3 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q4 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

| 2002Q1 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

| 2002Q2 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

| 2002Q3 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

N = 15

times = pd.date_range("2017-05-20 00:00", freq="1min", periods=N)

df = pd.DataFrame({"time": times,

"value": np.arange(N)})

df| time | value | |

|---|---|---|

| 0 | 2017-05-20 00:00:00 | 0 |

| 1 | 2017-05-20 00:01:00 | 1 |

| 2 | 2017-05-20 00:02:00 | 2 |

| 3 | 2017-05-20 00:03:00 | 3 |

| 4 | 2017-05-20 00:04:00 | 4 |

| 5 | 2017-05-20 00:05:00 | 5 |

| 6 | 2017-05-20 00:06:00 | 6 |

| 7 | 2017-05-20 00:07:00 | 7 |

| 8 | 2017-05-20 00:08:00 | 8 |

| 9 | 2017-05-20 00:09:00 | 9 |

| 10 | 2017-05-20 00:10:00 | 10 |

| 11 | 2017-05-20 00:11:00 | 11 |

| 12 | 2017-05-20 00:12:00 | 12 |

| 13 | 2017-05-20 00:13:00 | 13 |

| 14 | 2017-05-20 00:14:00 | 14 |

df.set_index("time").resample("5min").count()| value | |

|---|---|

| time | |

| 2017-05-20 00:00:00 | 5 |

| 2017-05-20 00:05:00 | 5 |

| 2017-05-20 00:10:00 | 5 |

df2 = pd.DataFrame({"time": times.repeat(3),

"key": np.tile(["a", "b", "c"], N),

"value": np.arange(N * 3.)})

df2.head(7)| time | key | value | |

|---|---|---|---|

| 0 | 2017-05-20 00:00:00 | a | 0.0 |

| 1 | 2017-05-20 00:00:00 | b | 1.0 |

| 2 | 2017-05-20 00:00:00 | c | 2.0 |

| 3 | 2017-05-20 00:01:00 | a | 3.0 |

| 4 | 2017-05-20 00:01:00 | b | 4.0 |

| 5 | 2017-05-20 00:01:00 | c | 5.0 |

| 6 | 2017-05-20 00:02:00 | a | 6.0 |

time_key = pd.Grouper(freq="5min")resampled = (df2.set_index("time")

.groupby(["key", time_key])

.sum())

resampled

resampled.reset_index()| key | time | value | |

|---|---|---|---|

| 0 | a | 2017-05-20 00:00:00 | 30.0 |

| 1 | a | 2017-05-20 00:05:00 | 105.0 |

| 2 | a | 2017-05-20 00:10:00 | 180.0 |

| 3 | b | 2017-05-20 00:00:00 | 35.0 |

| 4 | b | 2017-05-20 00:05:00 | 110.0 |

| 5 | b | 2017-05-20 00:10:00 | 185.0 |

| 6 | c | 2017-05-20 00:00:00 | 40.0 |

| 7 | c | 2017-05-20 00:05:00 | 115.0 |

| 8 | c | 2017-05-20 00:10:00 | 190.0 |

close_px_all = pd.read_csv("examples/stock_px.csv",

parse_dates=True, index_col=0)

close_px = close_px_all[["AAPL", "MSFT", "XOM"]]

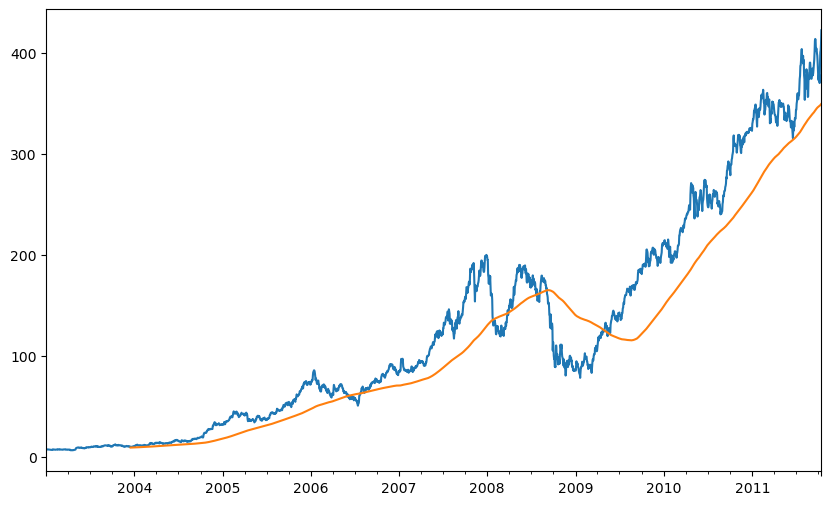

close_px = close_px.resample("B").ffill()close_px["AAPL"].plot()

close_px["AAPL"].rolling(250).mean().plot()

plt.figure()

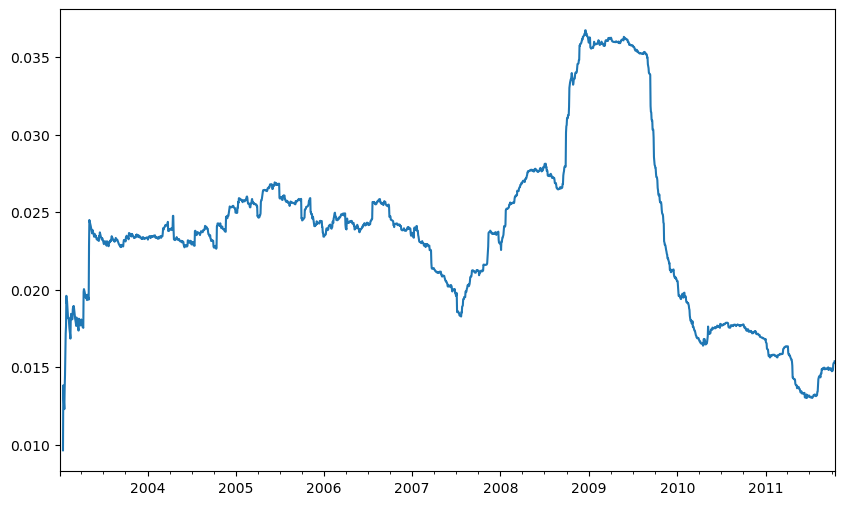

std250 = close_px["AAPL"].pct_change().rolling(250, min_periods=10).std()

std250[5:12]

std250.plot()

expanding_mean = std250.expanding().mean()plt.figure()<Figure size 1000x600 with 0 Axes><Figure size 1000x600 with 0 Axes>plt.style.use('grayscale')

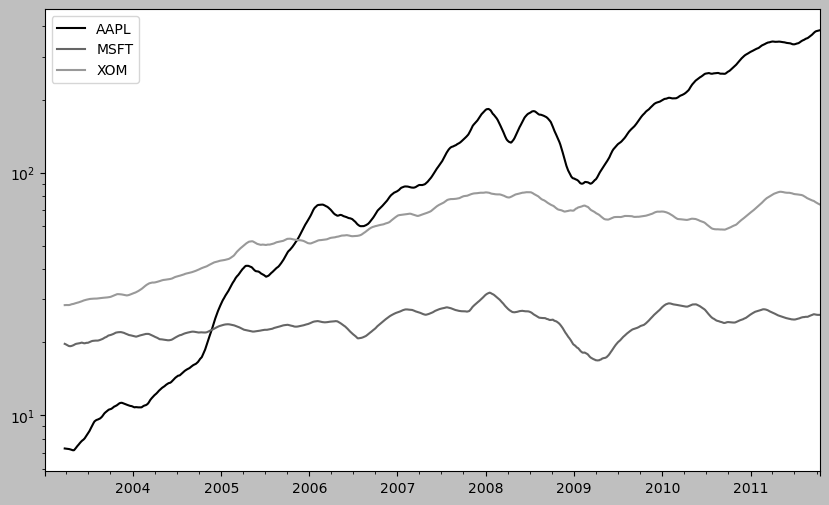

close_px.rolling(60).mean().plot(logy=True)

close_px.rolling("20D").mean()| AAPL | MSFT | XOM | |

|---|---|---|---|

| 2003-01-02 | 7.400000 | 21.110000 | 29.220000 |

| 2003-01-03 | 7.425000 | 21.125000 | 29.230000 |

| 2003-01-06 | 7.433333 | 21.256667 | 29.473333 |

| 2003-01-07 | 7.432500 | 21.425000 | 29.342500 |

| 2003-01-08 | 7.402000 | 21.402000 | 29.240000 |

| ... | ... | ... | ... |

| 2011-10-10 | 389.351429 | 25.602143 | 72.527857 |

| 2011-10-11 | 388.505000 | 25.674286 | 72.835000 |

| 2011-10-12 | 388.531429 | 25.810000 | 73.400714 |

| 2011-10-13 | 388.826429 | 25.961429 | 73.905000 |

| 2011-10-14 | 391.038000 | 26.048667 | 74.185333 |

2292 rows × 3 columns

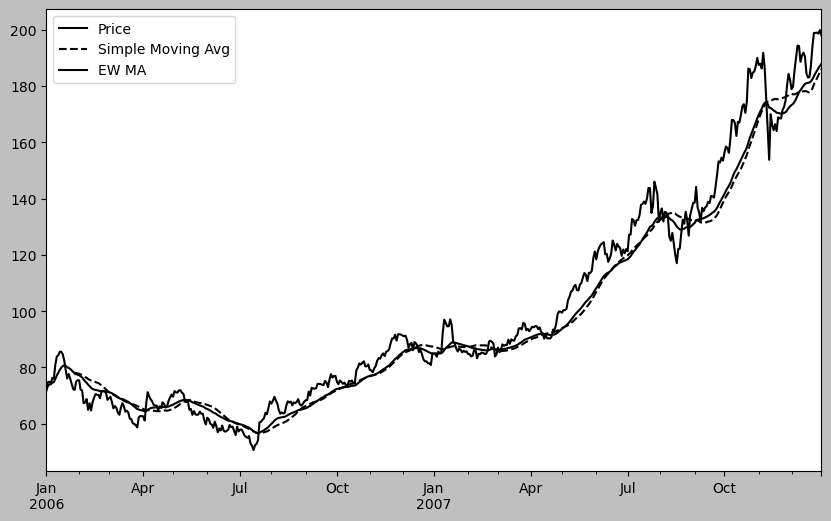

plt.figure()<Figure size 1000x600 with 0 Axes><Figure size 1000x600 with 0 Axes>aapl_px = close_px["AAPL"]["2006":"2007"]

ma30 = aapl_px.rolling(30, min_periods=20).mean()

ewma30 = aapl_px.ewm(span=30).mean()

aapl_px.plot(style="k-", label="Price")

ma30.plot(style="k--", label="Simple Moving Avg")

ewma30.plot(style="k-", label="EW MA")

plt.legend()

plt.figure()<Figure size 1000x600 with 0 Axes><Figure size 1000x600 with 0 Axes>spx_px = close_px_all["SPX"]

spx_rets = spx_px.pct_change()

returns = close_px.pct_change()corr = returns["AAPL"].rolling(125, min_periods=100).corr(spx_rets)

corr.plot()

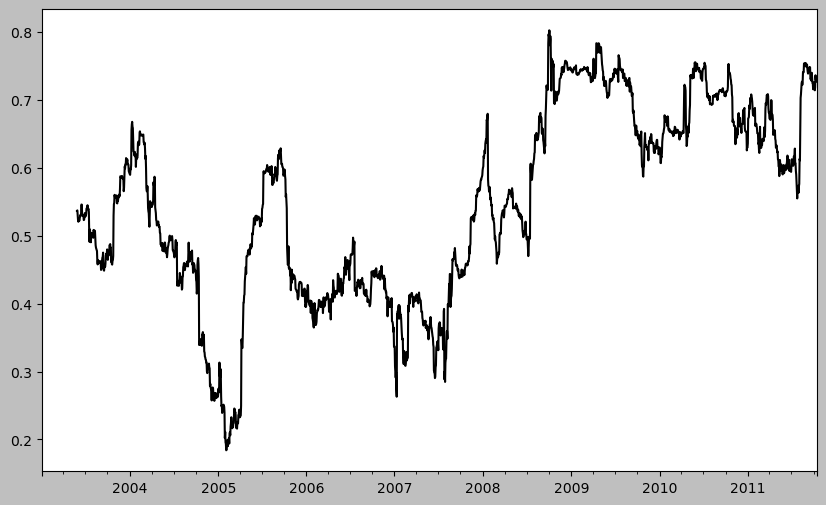

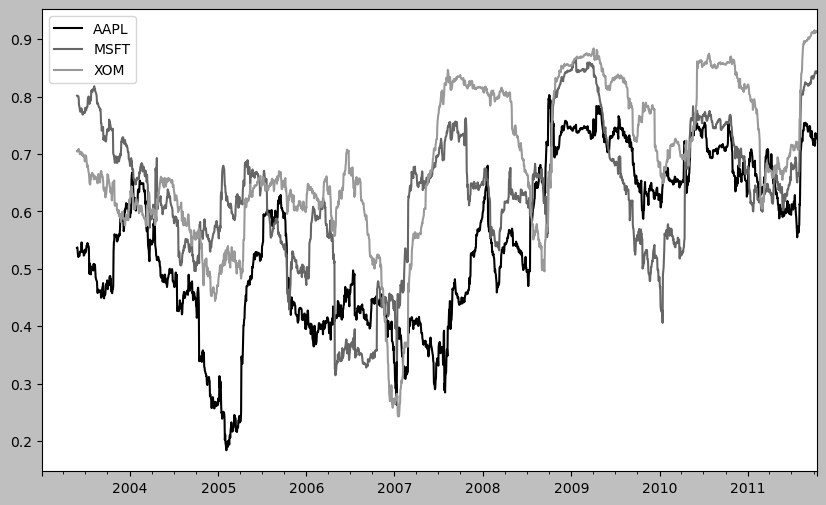

plt.figure()<Figure size 1000x600 with 0 Axes><Figure size 1000x600 with 0 Axes>corr = returns.rolling(125, min_periods=100).corr(spx_rets)

corr.plot()

plt.figure()<Figure size 1000x600 with 0 Axes><Figure size 1000x600 with 0 Axes>from scipy.stats import percentileofscore

def score_at_2percent(x):

return percentileofscore(x, 0.02)

result = returns["AAPL"].rolling(250).apply(score_at_2percent)

result.plot()

pd.options.display.max_rows = PREVIOUS_MAX_ROWS